I was sitting across from a 55-year-old client from West Des Moines last week who on the surface had done everything right with their retirement plan. He had been saving for decades, living within his means, and stuck to his plan during market swings. But he asked a question that highlighted one of the biggest values we provide our clients.

“I have $320k in my (taxable) brokerage account, $410 in my 401(k) and $120k in my Roth IRA. When I retire, how do I know which account to pull from first?”

In the grand scheme of things, this is one of the most important questions you can ask your financial advisor, not to mention one of the most valuable services they provide you. While there are some guiding principles, the answer to this question varies for every client and the sooner you ask it, the more flexibility you will have not only in how you withdraw it but as you are investing in them as well.

Why is it important to ask this question? Because getting it wrong can cost you tens of thousands of unnecessary taxes, higher Medicare premiums, and a smaller legacy to pass on to your heirs. This is one of the foundational services we provide at RetireRight as there are few conversations that will have a bigger impact on your financial future.

Why Everyone’s Situation is Different

Every account has a different job to do. Some were built for flexibility. Others for deferring taxes or long-term, tax-free growth. The mistake many people make is treating them as a single entity rather than three distinct tools, each with its own rules, tax rules, and purpose.

Let’s take quick look at how each account works:

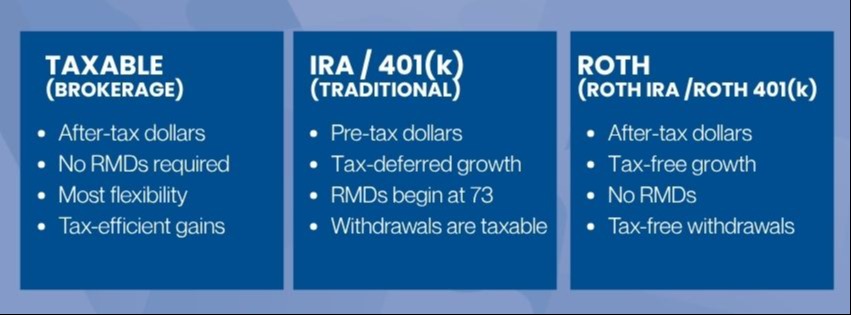

- Taxable brokerage accounts hold after-tax dollars. You have already paid income tax on the money you invested and will need to pay capital gains tax when you sell. There are no required minimum distributions (RMDs), nor penalties for withdrawing from these accounts early. While not tax advantageous, these accounts provide the most flexibility of the three.

- Traditional IRA and 401(k) accounts are funded with pre-tax dollars, which means every withdrawal is taxed as ordinary income. They grow tax-deferred, which is a powerful feature during your working years, but RMDs will kick in at age 73 and can push you into a higher tax bracket if left unmanaged.

- Roth accounts (Roth IRA or Roth 401(k)) use after-tax dollars, grow tax-free, and qualified withdrawals are completely tax-free in retirement, provided certain conditions are met. There aren’t any RMDs from a Roth IRA, making it an excellent long-term investment vehicle.

The question isn’t so much which account you should use first but rather in what order and why. And the answer to those questions is guided by your specific situation and goals. It’s this sequence that matters, as coordinating these accounts today can maximize their impact in the future.

The Five Factors That Shape Your Sequence

For our client with $850,000 spread across three accounts, the stakes were real. The withdrawal sequence we created will ripple through five aspects of his finances, some of which he had never considered before.

1. Taxes

Every dollar you pull from a traditional IRA or 401(k) is taxed as ordinary income. Pull too much in a single year, and you could move into a higher tax bracket. For Iowa retirees, there is an additional advantage as Iowa does not tax retirement income, so federal tax planning carries even more weight. Strategic withdrawals from your taxable account or Roth in the right years can keep your taxable income lower and lower your tax bill.

2. Future RMDs

Many people underestimate how large their required minimum distributions will be by age 73. If you spend down your taxable and Roth accounts first and leave a $600,000 traditional IRA untouched for 15 years, the mandatory withdrawals could be substantial and taxable. Thoughtful early distributions, or Roth conversions in the years before RMDs begin, can significantly reduce that future burden

3. Medicare Premiums

Most retirees do not realize that their income directly affects what they pay for Medicare. The Income-Related Monthly Adjustment Amount, known as IRMAA, adds surcharges to both Part B and Part D premiums for people above certain income thresholds. A large IRA withdrawal in one year can trigger these surcharges the following year. Spreading income strategically across these account types can help keep you below those thresholds.

4. Social Security Taxes

Up to 85 percent of your Social Security benefits can be subject to federal income tax, depending on your "combined income" level. Pulling heavily from a traditional IRA raises that number. Using Roth or taxable accounts instead, in the right years, can keep more of your Social Security benefit tax-free. This is one of the most common things that catches people off guard when they see their first tax return in retirement.

5. Heirs and Your Legacy

The account you leave behind can matter as much as the one you spend down. Under current rules, a non-spouse beneficiary who inherits a traditional IRA must withdraw the entire account within 10 years and pay ordinary income tax on every dollar. By comparison, a Roth IRA passes income tax-free. So, if leaving a meaningful legacy is important to you, this distinction shapes the entire strategy.

The Sequence Matters: Here Is What It Looks Like in Practice

Going back to our client in Des Moines: once we mapped out how his three accounts connected to each of those five factors, the picture changed completely. The conversation was no longer about which account to touch first. It became about creating a coordinated multi-year plan. A plan that considered his tax bracket each year, when to start Social Security, how to manage his IRA balance before age 73, and what he wanted to leave behind for his family.

That plan looked different from what a neighbor with the same account balance might do. Retirement planning is not one-size-fits-all, and the sequence of withdrawals is where generic advice can do real damage.

How RetireRight Approaches Sequencing

We work with families across West Des Moines, Dubuque, and the entire Midwest to navigate these types of questions. The people we serve have worked hard, saved consistently, and built something real. Our job is to make sure the distribution phase of retirement is as well orchestrated as the accumulation phase was.

Frequently Asked Questions

Which retirement account should I withdraw from first?

There is no single right answer as it depends on your tax bracket, age, Social Security timing, Medicare exposure, and legacy goals. Most retirees benefit from a coordinated strategy that draws from different account types in different years rather than depleting accounts one at a time.

Should I use my Roth IRA last?

Often, yes, but not always. Roth accounts grow tax-free and have no RMDs, which makes them valuable to preserve. However, there are situations where strategic Roth withdrawals earlier in retirement make sense, particularly to manage taxable income in lower-income years.

How do I know if I need help with withdrawal sequencing?

If you have savings in more than one type of retirement account and are within 10 years of retirement or already retired, a coordinated withdrawal strategy is worth a conversation. The earlier you start planning, the more options you have.

Let's Talk About Your Accounts

If you have been wondering which bucket to draw from first or whether your current approach is leaving money on the table we are here to help. RetireRight serves individuals and families across Iowa from our offices in West Des Moines and Dubuque, and this conversation is one of the most valuable ones we have with our clients.

Reach out at uretireright.com or call our office at 866-379-4015 to schedule a review. There is no obligation, and you might be surprised how much a clearer withdrawal sequence can change your retirement picture.

This material describes a hypothetical situation based on real life examples. Circumstances have been changed. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.